The smartphone market has reached saturation point in mature markets with the lowest level of shipments in the industry's short history

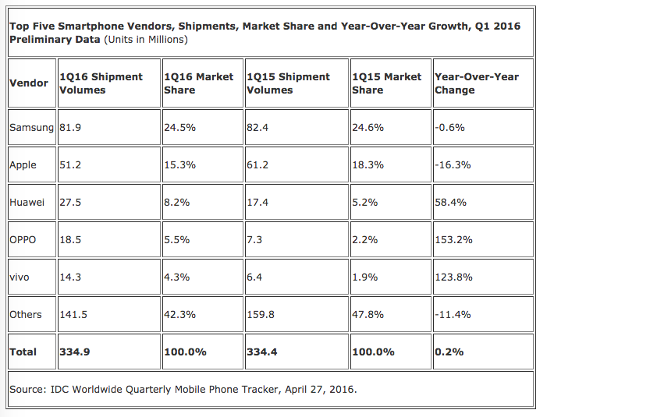

Smartphone shipments worldwide flattened out in the first quarter of 2016, with just 0.2pc growth year-on-year, the smallest growth on record.

The two market leaders, Apple and Samsung, saw the biggest decline.

In an interesting development, little-known Chinese brands OPPO and Vivo pushed Lenovo and Xiaomi out of the top five.

Overall, some 334.9m smartphones were shipped in the first quarter of 2015.

IDC attributed the tiny 0.2pc growth rate to smartphone saturation in developed markets, as well as year-on-year decline from both Apple and Samsung.

Samsung remained the leader in the worldwide smartphone market despite a year-over-year decline of 0.6pc in shipments. Despite the slight decline, the new Galaxy S7 and S7 edge sold vigorously in the month of March and were helped by numerous enticing carrier promotions to help push volume.

Apple could yet bounce back

This week, Apple reported its first quarterly decline in iPhone shipments in the iPhone’s nine-year history as volumes slipped to 51.2 million units, down 16.3pc from last year.

IDC reckons that, despite the plethora of new features found in the newer S models, current iPhone 6 and 6 Plus owners feel that an upgrade is not yet warranted.

The launch of the iPhone SE, which has all the power of the 6S in a compact form factor, could help, but at $399 the SE features equally powerful competition from competitors in India and China.

It is envisaged the SE will begin having an impact on iPhone shipments in the second quarter of 2016.

Smartphone market peaks in China, falls off a cliff

The biggest change to the market is the smartphone market in China passing its peak.

In 2013, China’s year-over-year shipment growth was 62.5pc; by 2015, it had dropped to 2.5pc.

“Along China’s maturing smartphone adoption curve, the companies most aligned with growth are those with products serving increasingly sophisticated consumers,” said IDC senior research manager Melissa Chau.

“Lenovo benefited with average selling prices (ASPs) below $150 in 2013, and Xiaomi picked up the mantle with ASPs below $200 in 2014 and 2015.

“Now Huawei, OPPO and Vivo, which play mainly in the sub-$250 range, are positioned for a strong 2016. These new vendors would be well-advised not to rest on their laurels though, as this dynamic smartphone landscape has shown to even cult brands like Xiaomi that customer loyalty is difficult to consistently maintain.”

Outside of China, many of these brands are virtually unknown and the ability of these rapidly-growing Chinese vendors to gain entry into mature markets such as the US and western Europe will be essential if they have aspirations of catching Apple or Samsung at the top, IDC said.

“Huawei has proven that it can sell increasingly premium devices,” said IDC research manager Anthony Scarsella.

“In China, Huawei is already recognised as a premium brand, but it is now going toe-to-toe on build quality with premium devices like the Nexus 6P that are available worldwide. While Huawei is furthest along in terms of international recognition, selling equally impressive volumes outside of China remains a challenge for many of these brands, whether it is Xiaomi, Lenovo, OPPO, or Vivo.

“Their ability to drive local growth no longer applies when it comes to international expansion, where premium branding quickly turns to price competition,” Scarsella said.

iPhone launch in China image via Shutterstock