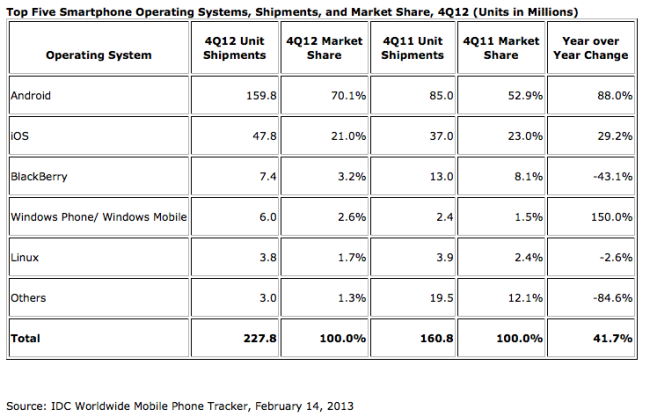

Google’s Android is the No 1 smartphone operating system in the world by volume, followed by Apple iOS. Between them, Android and iOS accounted for 91.1pc of smartphone shipments in the fourth quarter.

According to IDC, Android had a 70.1pc share of the world market with 159.8m smartphones shipped in Q4.

Apple’s iPhone had 21pc of the world smartphone market in Q4 with 47.8m smartphones shipped.

BlackBerry had 7.4pc of the global market, down 43pc on the previous year.

The dark horse to watch in 2013 is Microsoft, whose Windows Phone operating system saw a 150pc growth to 6m devices shipped in Q4, giving it a 2.6pc share of the global market.

Devices based on Linux had 1.7pc of the global market, with 3.8m Linux smartphones shipped in Q4.

For calendar year 2012, Android and iOS combined for 87.6pc of the 722.4m smartphones shipped worldwide, up from 68.1pc of the 494.5m units shipped during calendar year 2011.

“The dominance of Android and Apple reached a new watermark in the fourth quarter,” said Ramon Llamas, research manager with IDC’s Mobile Phone team.

“Android boasted a broad selection of smartphones, and an equally deep list of smartphone vendor partners. Finding an Android smartphone for nearly any budget, taste, size, and price was all but guaranteed during 2012. As a result, Android was rewarded with market-beating growth.

“Likewise, demand for Apple’s iPhone 5 kept iOS out in front and in the hands of many smartphone users,” added Llamas. “At the same time, lower prices on the iPhone 4 and the iPhone 4S brought iOS within reach of more users and sustained volume success of older models. Even with the Apple Maps debacle, iPhone owners were not deterred from purchasing new iPhones.”

Samsung was the biggest contributor to Android’s success, amassing 42.0pc of all Android smartphone shipments during the year. Following Samsung was a long list of vendors with single-digit market share, and an even longer list of vendors with market share less than 1pc.

Mid-year iPhone release likely

iOS posted yet another quarter and year of double-digit growth with strong demand for the iPhone. But what also stands out is how iOS’ year-over-year growth has slowed compared to the overall market. The smaller volumes during the second quarter of 2012 and to a smaller extent the third quarter underscore the possibility for a mid-year iPhone release in order to maintain market-beating growth.

Speculation about the release of possible larger-screen and inexpensive models during the middle of 2013 continues to follow Apple, which would help sustain growth. But until any model is formally announced, speculation remains simply that.

BlackBerry’s decision to postpone the release of BB10 to 2013 left the platform vulnerable in 2012 and reliant primarily on older smartphones running on BB7. As a result, BlackBerry’s tight grip on enterprise users has loosened and its popularity within emerging markets has been diminished by the competition. Now that BlackBerry has unveiled BB10, the company is faced with migrating current BlackBerry users to upgrade while persuading smartphone users of other platforms, including previous BlackBerry users, to switch.

Windows Phone/Windows Mobile made market-beating progress in Q4 and during 2012. The addition of Nokia’s strong commitment behind the platform was the key driver in Microsoft’s success. At the same time, the relationship has benefited Nokia, which amassed 76.0pc of all Windows Phone/Windows Mobile smartphone shipments. Beyond Nokia, however, is a short list of other vendors who have been experimenting with Windows Phone while also supporting Android.