Architectural detail of modern building in Potsdamer Platz, Berlin. Image: Vytautas Kielaitis/Shutterstock

European venture capital fundraising has reached a 10-year high of €8.8bn.

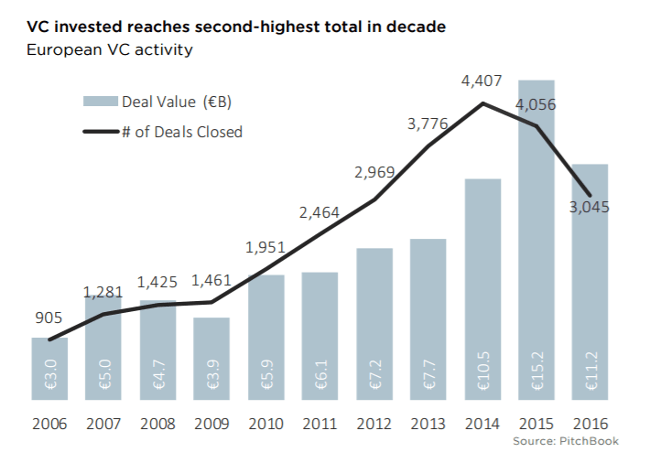

Despite Brexit and plummeting investment, venture capital (VC) fundraising in Europe has reached €8.8bn – the highest recorded in a decade.

But before anyone puts the champagne on ice, it’s the lowest number of funds closed since at least 2005.

There has been an overall decline in deals and money invested, according to PitchBook.

‘European VCs are raising fewer microfunds, making it more difficult for companies looking to secure their first round of institutional financing’

– NIZAR TARHUNI

In 2016, total deal value dropped by roughly €4bn from 2015, falling from €15.2bn – a 10-year high – to €11.2bn last year.

That €11.2bn was invested across 3,045 completed transactions.

While the number of funds are down, the amounts raised among respective funds is ballooning. For the first time in at least a decade, investors closed 11 funds valued at, or above, €250m.

Of those funds, three fell into the €500m-plus size bracket, including a £500m (€664m) fund raised by Cocoon Networks.

Angel and seed investments decline in Europe

Image: PitchBook

The problem is, however, that VCs are also writing bigger cheques for high-growth companies and investing less in seed-stage companies.

In 2016, only 908 first financings were completed in Europe – the fewest recorded since 2009.

European angel and seed investments also saw the steepest year-on-year decline of any other deal type in 2016, falling from 2,096 in 2015 to 1,356 last year.

“European VCs are raising fewer microfunds, making it more difficult for companies looking to secure their first round of institutional financing,” said Nizar Tarhuni, analysis manager at PitchBook.

“Instead, they appear to be raising larger funds and making bigger investments. We’re unsure as to why that is exactly, but we think European VCs are simply planning ahead. They want to ensure they’ve got capital on hand when it comes time to make follow-on investments in the later stages of the most promising companies.”

Despite the significant decline in deal activity last year, 2016 recorded the second-highest level of capital invested in the last decade. At the same time, as VCs raised larger funds, the median deal size increased 44pc year-on-year.

PitchBook reported that while certain parts of Europe – including central and eastern European countries – experienced a more dramatic drop-off in VC deal activity during 2016, the Nordic region, as well as Germany, Switzerland and Austria (DACH), continued to attract investors.

In 2016, 519 VC deals were completed in the Nordic region, down only 4pc from the year prior, while 470 deals were made in the DACH region, down 16pc from 2015.

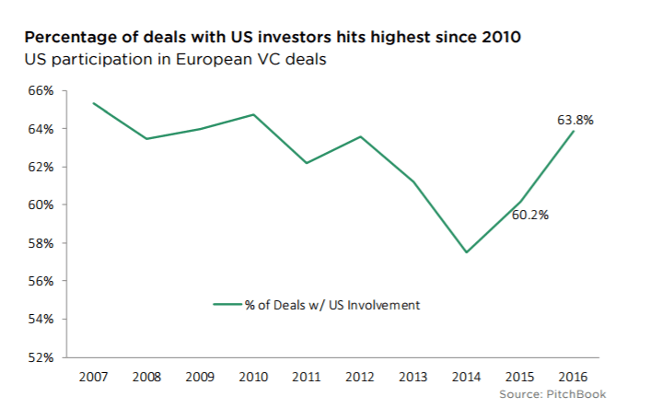

The PitchBook data also shows that US investors are still interested in Europe, as they participated in 1,944 VC deals in 2016. This was down by almost 500 from last year, but was still the highest percentage since 2010.

Image: PitchBook

In terms of total deal value, transactions involving US investors totalled €9.4bn, or 84pc of total deal value.

The majority of deals involving US investors were priced at or above €25m, demonstrating investors’ continued interest in late-stage companies, which includes investments into Global Fashion Group, Deliveroo and Farfetch.

Brexit and exits

While it’s difficult to know exactly how much Brexit has impacted the exit environment in Europe, the PitchBook data shows that only 26pc of total exit value was realised in the second half of 2016.

It said it is too early to draw conclusions surrounding the impact of Brexit on exit processes – especially since they can often take months, if not quarters, to complete.

Given the recent referendum decisions, active corporate acquirers will need to reassess where they’re going to put their money, which could have an impact on future M&A activity.

Modern building in Potsdamer Platz in Berlin. Image: Vytautas Kielaitis/Shutterstock