The Apple iPad

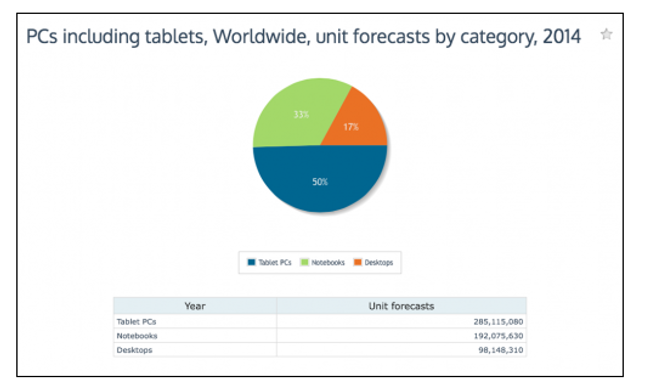

Next year tablet-styled devices will out-ship almost all other PC form factors combined, making up almost 50pc of the total PC market of desktops, notebooks and tablets.

A new forecast from Canalys found that the worldwide PC market grew 18pc in the third quarter of 2013, despite desktop and notebook shipments continuing to decline.

Tablet shipments accounted for 40pc of PC shipments in the third quarter, less than half a million units behind total notebook shipments.

Canalys forecasts that 285m units will ship in 2014, growing to 396m in 2017.

Apple and Samsung will continue to keep ahead of their competitors in the medium term but face challenges as competition heats up.

Apple

Apple maintained its top vendor position throughout 2013, and the launch of the iPad Air and new iPad mini will strengthen that position in Q4. Its desktop and notebook business has remained stable while other vendors have seen their shipments deteriorate. Apple’s prioritisation of protecting gross margins will see its PC market share continue to decline.

“Apple’s decline in PC market share is unavoidable when considering its business model. Samsung narrowly took the lead in EMEA this quarter and Apple will lose its position to competitors in more markets in the future,” said Canalys senior analyst Tim Coulling.

“However, Apple is one of the few companies making money from the tablet boom. Premium products attract high-value consumers; for Apple, remaining highly profitable and driving revenue from its entire ecosystem is of greater importance than market share statistics.”

Microsoft

Canalys forecasts that Microsoft will take 5pc of the tablet PC market in 2014, up from just 2pc in 2012.

“(The year) 2014 will see another major shift for the company as the Nokia acquisition brings it a step closer to being a fully-fledged smart mobile device vendor. As a vendor, Microsoft needs to prove to channel partners and consumers that it is in this market for the long haul. Balancing the competition with its vendor partners and embracing a ‘challenger’ rather than an ‘incumbent’ mentality is essential.

“To improve its position it must drive app development and better utilise other relevant parts of its business to round out its mobile device ecosystem,” said Canalys research analyst Pin Chen Tang.

“A critical first step is to address the co-existence of Windows Phone and Windows RT. Having three different operating systems to address the smart device landscape is confusing to both developers and consumers alike.”

Android

Android-derived operating systems will be responsible for driving growth in the market and are forecast to take 65pc share in 2014 with 185m units.

Samsung continues to lead with strong year-on-year growth coming from its broad tablet portfolio, and in Q3 2013 it had a 27pc share of Android tablet shipments. But with hundreds of small-to-micro brand vendors in established and high-growth markets and international players such as Acer, Asus, Lenovo, and HP, this market share statistic will also start to decline.

“With the cost and time-to-market advantages afforded by their Chinese supply chain, these small-to-micro brand vendors are eating up tablet market share,” said Shanghai-based analyst James Wang.

“Vendors such as Nextbook in the United States, and Onda and Teclast in the People’s Republic of China ship more units than some of the major international top-tier vendors in their home countries. The rise of small-to-micro brand vendors has proved that there is a demand in for entry-level Android tablets in every country and in every region.”

“Vendors such as Acer, Asus, HP, and Lenovo have all entered the price war, with entry-level products at sub-U$150 price points.